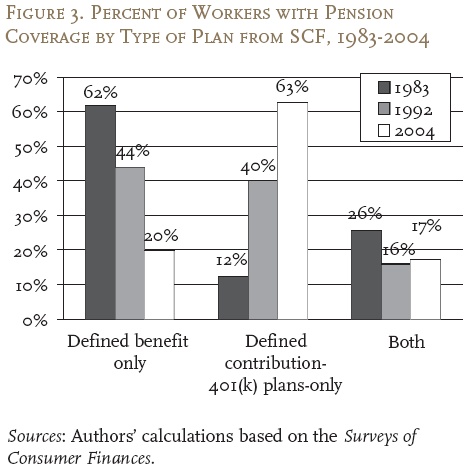

Good-bye to defined-benefit pension plans

Many large pension funds had models built on absurdly optimistic stock and bond market returns. These accounts did well in an era where the stock market roared ferociously because of the prime position the U.S. had after World War II. Those pension accounts are becoming a relic of the past:

Source: Surly Trader

This is a rather dramatic shift in events over the last 30 years. In 1983 62 percent of working Americans had some sort of defined benefit plan. In 2004 it was down to 20 percent and today it is lower. Americans have been forced to play the stock market game through their 401ks. This has actually turned out worse for average Americans as they try to compete with high frequency swindlers and investment banking crooks. Clearly someone is making profits as investment bankers pull down million dollar bonuses all the while the stock market has gone into reverse over a decade.

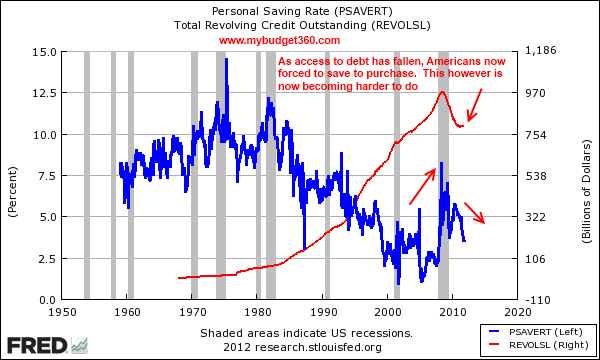

As access to debt declines Americans forced to use savings to consume

Since the end of World War II many Americans were given access to debt on an unparalleled level. This ability to borrow served as a supplement to a stagnant paycheck. As time has gone on and with the debt bubble bursting Americans have now seen their access to borrow severely curtailed:

It is no coincidence that as borrowing increased the savings rate went so low as to go into negative territory for a year. However, it has recently gone up not because of choice, but because the debt bubble has popped and now many need to actually save to purchase items. This has made the recovery extremely sluggish because saving to spend on a $25,000 income is hard to do. The typical household pulling in $50,000 will have a giant portion of their funds going to housing, food, energy, and healthcare before any discretionary spending is done.

Where does this leave retirement?

Many Americans rely completely on Social Security for their retirement. The idea of sipping unlimited Margaritas on some Caribbean island is largely a myth:

“(Market Place) Monrad is 73 years old. She has a bachelor’s degree and a master’s in linguistics, but she tended bar for most of her working life.

Monrad: I live on Social Security. I get $1,040 a month. So I don’t turn on my air conditioner. I’m dying of heat.”

Over 58,000,000 Americans receive some benefit from Social Security and most rely on this payment as their primary source of income in retirement. Remember that only one out of three Americans have even a penny to their name? Do you think the young with a tougher market are saving enough?

Source: CNN Money

“(CNN Money) In 1984, households headed by people age 65 and older were worth just 10 times the median net worth of households headed by people 35 and younger.

But now that gap has widened to 47-to-one, marking the largest wealth gap ever recorded between the two age groups.”

So the problem is only going to be exacerbated with this upcoming generation as they try to invest in their 401ks (if they can) into a stagnant and declining stock market. It is looking more and more that those assured 7 to 8 percent historical returns were largely a mathematical aberration thanks to a strong position after World War II. The big gains now are largely allocated to the well connected financial sector and our wealthier politicians that simply represent the interests of special lobbyists and groups. The new retirement is looking a lot like no retirement at all.